Intel Announces Q3 FY 2019 Earnings: Record Results

by Brett Howse on October 24, 2019 11:10 PM EST- Posted in

- CPUs

- Intel

- Financial Results

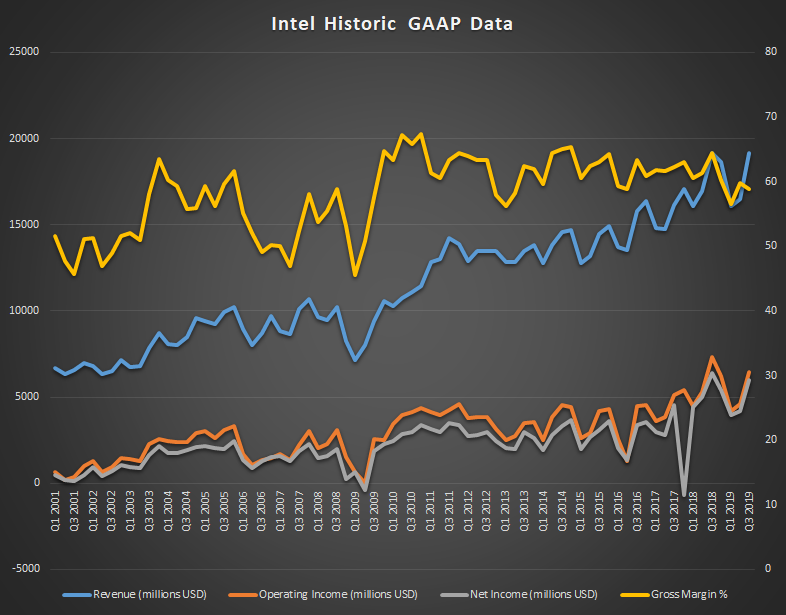

Today Intel announced their earnings for the third quarter of the 2019 fiscal year, which ended September 29, and the company has set a record for revenue thanks to increased growth of their datacenter business. Revenue for the quarter came in at $19.2 billion, beating Q3 2018 by $27 million, which results in a mere 0.14% growth over last year, but enough to make this the highest revenue ever for the company. Gross margin was 58.8%, down from 64.5% a year ago. Operating income was down 12% to $6.4 billion, and net income was down 6% to $6.0 billion. This resulted in earnings-per-share of $1.35, down 2% from a year ago.

| Intel Q3 2019 Financial Results (GAAP) | |||||

| Q3'2019 | Q2'2019 | Q3'2018 | |||

| Revenue | $19.2B | $16.5B | $19.2B | ||

| Operating Income | $6.4B | $4.6B | $7.3B | ||

| Net Income | $6.0B | $4.2B | $6.4B | ||

| Gross Margin | 58.9% | 59.8% | 64.5% | ||

| Client Computing Group Revenue | $9.7B | +10% | -5% | ||

| Data Center Group Revenue | $6.4B | +28% | +4% | ||

| Internet of Things Revenue | $1.0B | +1% | +9% | ||

| Mobileye Revenue | $229M | +14% | +20% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +38% | +19% | ||

| Programmable Solutions Group | $507M | +3.7% | +2% | ||

Intel splits their business into two main areas. The Client Computing Group is the PC-Centric products, and the Data Center Group consists of everything else. Despite the contraction of the PC market over the last several years, it has continued to be the main source of revenue for Intel, and that continues this quarter as well, but only by a small margin. The Client Computing Group revenue was down 5% year-over-year to revenue of $9.7 billion. Intel attributes this drop to lower year-on-year platform volume, although loss was partially offset by some of the higher-cost products especially in the commercial segment.

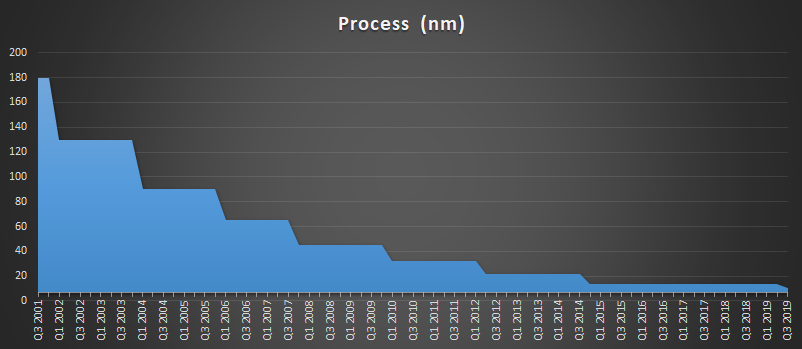

Although the overall PC side from Intel was down, Intel has only just launched their latest 10th generation Core products which won’t make up much of Q3’s numbers due to the cut-off date of the end of September. Intel now has over 30 devices launched based on the 10 nm Ice Lake platform, signalling the end of 14 nm which has been iterated on many times over the last several years as Intel struggled to get their 10 nm process off the ground. The good news for Intel is that despite the initial setbacks for 10 nm, they have stated that 10 nm yields are actually ahead of their internal expectations for this point in its lifecycle, which should help alleviate some of the backlog the company has been facing with production assuming the can use the improved yields to transition more of their lineup over to 10 nm a bit quicker. Intel has also stated that despite the years lost on 10 nm, they are moving back to a 2 to 2.5 year process cadence, with 7 nm on track for their GPU lineup in 2021.

Intel lumps the rest of their business into the “Data-Centric” role, and this side of the company has been making strong gains over the last several years, and now almost matches the Client Computing Group in total revenue at $9.5 billion, versus $9.7 billion for the CCG. But Data-Centric includes not only the Data Center Group, but also Internet of Things, Mobileye, Non-Volatile Storage, and Programable Solutions. Altogether these segments achieved record revenue, up 6% from 2018. Individually, Data Center Group was up 4% to $6.4 billion with a strong mix of Xeon sales and growth in all segments. Internet of Things also had record revenue, up 9% to $1.0 billion. Mobileye is also on the record train, with a 20% year-over-year gain to $229 million, as did Non-Volatile Storage which was up 19% to $1.3 billion. Programable Solutions was the only segment in the Data-Centric listings to not hit a record in revenue, but it was still up 2% to $507 million for the quarter, and they shipped their first 10 nm Agilex FPGA this quarter as well.

Looking ahead to Q4, Intel is expecting revenue around $19.2 billion with earnings-per-share of $1.28.

Source: Intel Investor Relations

39 Comments

View All Comments

Potato Power - Thursday, October 24, 2019 - link

Look at Intel has so much trouble with their 10nm. I won't bet on them to have 7nm ready in 2021. While TSMC will enter mass production for 5nm, ha.Cliff34 - Friday, October 25, 2019 - link

The bottom line is profit. Intel is still going strong despite AMD chipping some of their share.The question is how long will this last. Can Intel stay competitive in the next few years.

deepblue08 - Friday, October 25, 2019 - link

I am certain Intel will remain competitive. Keep in mind that they are a giant with deep pockets, they may be feeling the burn now, but this has happened in the past when AMD released Athlon64. I am more worried for AMD, they are doing very well now and I hope they don't take their foot off the pedal like they did after Athlon64.tiwi1391 - Friday, October 25, 2019 - link

AMD should have taken off with Athlon64 and become a bigger competitor, with more money for research and development. Except that Intel gave OEMs deal where they got special pricing for only selling Intel processors. AMD didn't take their foot off the pedal, Intel cut the gas line.Even if the market isn't as susceptible to the practices Intel used in the pre-Core days, you are right that AMD will have to continue innovating to try and get market share...

AshlayW - Saturday, October 26, 2019 - link

This. Intel is historically a scumbag company.Korguz - Saturday, October 26, 2019 - link

and it ended up costing them, a lotTheJian - Monday, October 28, 2019 - link

ROFL. I hope you don't mean it cost Intel a lot...1.5B when you made 60B over the 10yrs you screwed them, means I'll do it to you AGAIN, AND AGAIN, AND AGAIN.Do not expect Intel or MSFT to not act exactly as they have before because they are still monopolies. If you fine me 1.5b (heck 10B) every time I make 60B in 10yrs, I'll keep doing it as the fine means nothing but MORE profit for me while I bankrupt you (or whoever is next in line) over and over.

Business is WAR. Any bean-counter worth his salt should be able to figure out 60B NET is a lot higher than 1.5B after a 10yr legal war. I'll take that fine yearly for those 10yrs and it's STILL worth breaking the laws. 15B over 10yrs is still NOTHING compared to keeping the other 45B and your competition for getting ANY income (SEE AMD Q reports for 15yrs, they lost 8B over the life of the company!).

It appears Intel is doing the same thing as last time AMD was ahead. Announced 3B in payoffs. Kind of sounds EXACTLY like before right? "Don't use AMD you get X check". It will be interesting to see if we end up with ASUS boards in white boxes again with no ASUS silkscreen on boards at all like before. I truly hope AMD has figured out some defense for this that won't take 10yrs to get a verdict again and a piss poor 1.5B that some IDIOT at AMD accepted. They should have sued until it was 1/2 of that 60B or more. They chose to settle, instead of waiting for a jury to rule for a BIG hit. Continuing the suit is cheap compared to what they lost and what they taught Intel (do it again, it's a cheap fine).

Amandtec - Friday, October 25, 2019 - link

You can coast off the brand loyalty from 'late adopters'. For example, my extended family would only ever buy Intel for the same reason they buy iPhones and Nike, they are the brand names they recognize. However, if you fast forward a decade this free lunch often comes to an end.FreckledTrout - Friday, October 25, 2019 - link

Agree. I hope AMD realizes this and starts doing some rather profesional marketing. They need there "Intel Inside" moment of marketing.Irata - Friday, October 25, 2019 - link

The sad thing about their record profits is that a nice part of this will probably go to stifling competition via various kickback / incentive schemes. This is what allowed them to stay competitive in the P3 / P4 days (until Core CPU were released) and I am really hoping that this time around it won't work.